What to do if your roof insurance claim is denied in oklahoma

Was your insurance claim denied? More specifically, did State Farm deny your insurance claim?

In Oklahoma, storms are often violent and unpredictable. From hail and straight-line winds to tornadoes and driving rain, severe weather can damage a roof in minutes—sometimes in ways that aren’t visible from the ground. As a result, when you file a claim expecting help and instead receive a denial letter, the experience is often frustrating, confusing, and stressful.

If your roof insurance claim was denied in Oklahoma, you’re not alone. Denials happen for a handful of common reasons—“cosmetic damage,” “wear and tear,” “no storm damage found,” “below deductible,” or “late notice” and many homeowners receive similar language from large carriers, including State Farm.

Here’s the good news: a denial is not always the end of the road. In many situations, homeowners can request a reinspection, submit additional documentation, escalate the claim, or seek a professional or legal review of the denial especially when the condition of the roof doesn’t match what the denial letter suggests.

This guide explains what to do next, step by step. It also includes practical checklists, sample wording, and documentation tips that can help you turn a “no” into a fair review—whether your carrier is State Farm or someone else.

Disclaimer: This article is provided for educational purposes only and does not constitute legal advice. Insurance policies and claim outcomes vary. If you require legal advice, please consult a licensed Oklahoma attorney.

schedule a free inspection today

Why Roof Insurance Claims Get Denied in Oklahoma (Common Reasons)

In many cases, roof claim denials in Oklahoma tend to fall into a few common patterns. By understanding the specific category involved, homeowners can more effectively build a smart, informed response.

1) “Cosmetic Damage Only” (Most Common After Hail)

Many carriers—including State Farm—may describe hail impacts as “cosmetic” when the roof is not leaking or when the adjuster concludes the roof is still “functional.”

Common denial language:

- “No functional impairment observed.”

- “Hail impacts are cosmetic.”

- “Roof remains serviceable.”

- “Damage does not affect water shedding.”

The problem is that hail can cause functional deterioration without immediate leaks. Bruised shingles can fail sooner, lose granules, crack later in heat/cold cycles, or lose their sealing strength—especially in Oklahoma’s harsh climate.

2) “Wear and Tear” / “Deterioration” / “Maintenance”

Another frequent denial reason is that the carrier attributes roof issues to age or long-term wear instead of storm damage. You may see:

- “Normal wear and tear.”

- “Granule loss consistent with age.”

- “Brittle shingles.”

- “Improper installation or maintenance.”

Even when a roof is older, a storm can still cause new, covered damage. The dispute becomes about causation and documentation—not just roof age.

3) “No Storm Damage Found” / “Insufficient Evidence”

Sometimes adjusters conclude:

- “No hail hits present.”

- “Wind damage not observed.”

- “Damage not consistent with reported storm.”

In real life, hail can be highly localized. One block in Oklahoma City can get hit while another doesn’t. A short inspection can also miss damage on certain slopes or at higher elevations.

4) “Below Deductible”

This isn’t always a total denial. The carrier may acknowledge damage but estimate repairs below your deductible, resulting in $0 payment. In many cases, homeowners dispute the scope—especially if:

- multiple slopes show damage,

- collateral items (vents, flashing, gutters) were ignored,

- labor or steep charges were undervalued.

5) Late Reporting / “Prompt Notice”

Some policies require “prompt notice” or impose time limits. Homeowners often delay because the roof isn’t leaking. But delayed reporting can lead to pushback like:

- “Damage could not be verified due to late notice.”

- “Cannot confirm storm causation.”

Late notice doesn’t automatically mean you’re out of options, but it increases the importance of well-organized documentation.

Step 1: Don’t Panic—Read the Denial Letter Like a Contractor (or Lawyer) Would

At its core, the denial letter serves as a roadmap. Your next step, therefore, is to carefully identify exactly what the insurer is asserting and what evidence it relied upon in reaching its decision.

When State Farm denies a roof claim, the letter often includes:

- A summary of inspection findings

- A reference to coverage sections or exclusions

- A conclusion such as “cosmetic only,” “wear and tear,” or “no storm damage”

What to look for in your roof claim denial letter:

- Claim number

- Date of loss (storm date) the insurer is using

- Reason for denial (the key phrase)

- Policy language cited (coverage vs exclusions)

- Whether it’s a full denial or a partial approval / below deductible

What to do immediately:

- Save the letter as a PDF

- Screenshot it on your phone as a backup

- Create a folder titled:

Roof Claim – [Carrier] – [Date of Loss] – Denial

If your carrier is State Farm, label your folder clearly. Organization matters later.

Step 2: Request the Full Claim File (Yes, Ask for Their Photos Too)

If you want to challenge or review a denial, you need to see what the carrier saw—and what they documented.

Request:

- Adjuster report (field notes)

- All photos taken

- Any roof measurements or diagrams

- The estimate (even if the total is $0)

- Any internal claim summaries provided to you

Why this matters:

Many denials are based on limited photos or a quick inspection that missed key evidence. If you don’t request the full file, you’re arguing in the dark.

Sample wording you can email (simple and professional):

“Please provide, at your earliest convenience, the complete claim file for claim number ______, including but not limited to the adjuster’s report, all photographs, measurements, notes, and any estimates or scope documents related to the denial.”

If it’s State Farm, keep it calm and factual—this is a business request.

Step 3: Schedule an Independent Roof Inspection (This Is the Turning Point)

Most denied roof claims that later get approved are reversed because the homeowner brings better documentation than the initial inspection produced.

You want an inspection that includes:

- Slope-by-slope photos (each roof plane)

- Close-up hail/wind indicators

- Collateral damage photos (vents, flashing, gutters, metal edges)

- Notes identifying patterns (not just “hail present”)

- A short written summary that ties findings to the storm

What does a good contractor look for after a roof insurance claim is denied in oklahoma?

Hail indicators

- bruise marks, fractures, granule displacement patterns,

- consistent impact spacing,

- collateral hits on soft metals.

Wind indicators

- creased shingles,

- lifted tabs,

- broken seal strips,

- exposed fasteners or missing shingles.

Why collateral damage matters:

If a roof has “no storm damage,” you often still see evidence on:

- turtle vents,

- ridge caps,

- metal drip edge,

- gutters and downspouts,

- flashing.

Collateral damage can support storm intensity and consistency.

schedule a free inspection today

Step 4: Build a “Claim Story” That Makes Sense

Insurance decisions are documentation decisions. Your goal is to present a clear story:

- A storm occurred on X date

- The roof shows damage consistent with that storm

- The damage is not just cosmetic (or is disputed)

- Collateral components show storm impacts

- The scope needed is reasonable and tied to roofing standards

This doesn’t need to be dramatic. It needs to be organized.

Your documentation packet should include:

To begin, start with the denial letter, as it outlines the insurer’s stated reasoning. Next, review the claim file photos provided by the insurer, including, where applicable, photos from State Farm. In addition, gather and organize all contractor photos to clearly show consistent damage patterns. From there, prepare a concise, one-page inspection summary that explains the findings in plain terms. Optionally, you may also include a general weather report screenshot for context—not as proof, but as supporting background. Finally, if emergency mitigation was performed, invoices for services such as tarping can further help document the timeline and necessity of repairs.

Step 5: Respond to the Denial Based on the Specific Reason

Different denials require different responses.

If State Farm says “Cosmetic Only” after a denied insurance claim

Your response should focus on:

- functional impairment indicators (fractures, bruising, compromised shingle integrity),

- consistent damage patterns across slopes,

- collateral impacts.

Also request clarification:

- What standard did they use to define “functional” vs “cosmetic”?

- Which slopes were inspected and documented?

If State Farm says “Wear and Tear”

Your response should focus on:

- storm causation evidence,

- clear photos of impacts consistent with hail/wind,

- explanation that the claim is for storm-related damage, not old age.

If State Farm says “No Damage Found” as a reason to deny your roof claim

Your response should focus on:

- slope-by-slope evidence,

- collateral components,

- request for reinspection with a different adjuster or supervisor.

If State Farm says “Below Deductible”

Your response should focus on:

- First, conduct a scope comparison by reviewing the estimate line by line to identify discrepancies.

- Next, note any missing line items, such as steep charges, ridge cap, starter strip, or vents, that may not have been accounted for.

- Additionally, evaluate any applicable code-related requirements, as these obligations can materially affect the scope and cost of repairs.

- Finally, use these findings to submit a clear, well-supported supplement request for proper consideration.

Step 6: Request a Reinspection (The Right Way) after a denied roof claim

This is where most homeowners lose momentum. They call, complain, and get nowhere. Instead, submit a clean request with attachments.

What to include:

- To begin, clearly reference the claim number and date of loss to ensure the request is properly identified.

- Next, include a concise, one-paragraph summary explaining what was missed or is being disputed.

- From there, attach the supporting documentation, including relevant photos and the inspection summary, to clearly illustrate the issues.

- Finally, formally request a reinspection and/or a supervisor review to allow the carrier an opportunity to reconsider the findings.

Sample reinspection request (copy/paste):

“We respectfully request a reinspection and supervisor review for claim ______. An independent inspection identified storm-related roof and collateral damage that does not appear fully documented in the original inspection. Attached are photos and an inspection summary for review. Please confirm next steps for scheduling a reinspection.”

If the carrier is State Farm, this tone is ideal: firm, neutral, documented.

Step 7: Meet the Adjuster With Your Contractor (If Allowed)

Many homeowners get better outcomes when the contractor attends the reinspection—not to argue, but to document.

A good contractor will:

- point out specific test areas,

- show collateral damage locations,

- keep the inspection moving,

- avoid emotional conflict.

Pro tip:

Ask your contractor to bring:

- a roof sketch with marked slopes,

- printed photos or a shared folder,

- a short summary of disputed findings.

schedule a free inspection today

Step 8: Escalate Within the Insurance Company (Supervisor Review)

If the reinspection still results in denial or minimal scope, request escalation:

- supervisor review,

- desk adjuster review,

- written response to your submitted evidence.

What you want in writing:

- Which slopes were inspected

- Why your documented evidence was rejected

- Which policy language supports their position

When State Farm knows you’re organized and keeping a paper trail, the claim is often handled more carefully.

Step 9: Understand Your Options if State Farm Still Denies the roof Claim

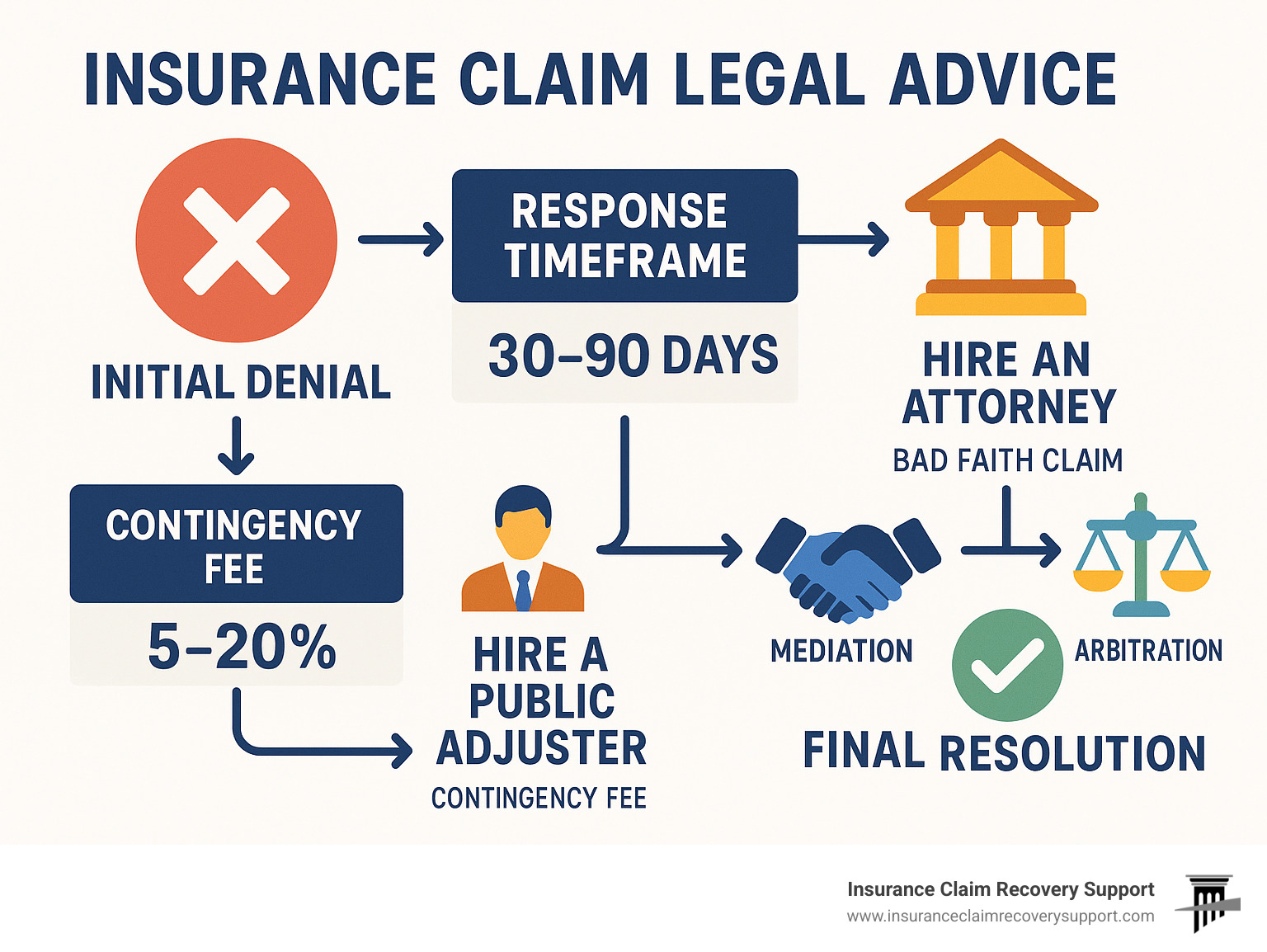

If you’ve documented the roof thoroughly and still get stonewalled, you have options. These vary by policy and situation, but here are the common paths:

Option A: Supplement Request (Scope Dispute)

If coverage exists but the scope is too small, a supplement may be appropriate. This is often used when the carrier paid something but missed key items.

Option B: Formal Complaint (Consumer Process)

Homeowners can file complaints through appropriate state channels if they believe a claim is handled unfairly. This does not guarantee payment, but it can trigger review.

Option C: Attorney Review (When It Becomes Necessary)

If you have strong evidence and repeated denials, some homeowners consult an Oklahoma attorney experienced with insurance disputes.

An attorney can:

- review policy language,

- assess denial reasoning,

- send a demand letter requesting compliance with the policy,

- guide next steps if the carrier refuses to properly evaluate evidence.

This step is situation-dependent. It’s not required for every claim, but it’s one way homeowners pursue fairness when the process stalls.

Again: not legal advice—just an educational overview.

Documentation Checklist: What Homeowners Should Gather After a roof claim Denial

Use this checklist for denied roof claims in Oklahoma (including State Farm):

Core documents

- To start, review the denial letter, as it explains the carrier’s stated basis for the decision.

- Next, reference the policy declarations page to confirm the applicable coverages and limits.

- At the same time, be sure to note the claim number and date of loss to ensure all correspondence is properly tied to the correct file.

- From there, request a copy of the adjuster’s report to understand the findings relied upon.

- Finally, ask the carrier to provide all claim-related photos, as these images often play a key role in how the denial was evaluated.

Photos and inspection evidence

- To begin, document the entire roof by capturing full photos of each slope to establish overall condition.

- Next, include clear close-ups of any suspected hail or wind damage to highlight specific impact areas.

- In addition, photograph related components such as vents, flashing, and gutters, as damage to these items can help support storm-related findings.

- Where applicable, add photos of any missing or lifted shingles to demonstrate functional damage.

- Finally, tie everything together with a concise written inspection summary, typically one to two pages, that explains the observations and conclusions in clear, organized terms.

Communication records

- Emails and letters with dates

- Names and titles of representatives

- Notes after phone calls (date/time + summary)

If emergency mitigation occurred

- Tarping photos (before/during/after)

- Invoices and receipts

- Reason for emergency action

Common Mistakes That Hurt Denied Roof Claims (Avoid These)

Mistake 1: Overreacting and stopping the process

Many homeowners assume the denial is final. Often it’s not—especially with better documentation.

Mistake 2: Not requesting the claim file

If you don’t see what State Farm documented, you can’t identify gaps.

Mistake 3: Unorganized photo dumps

In practice, sending 150 unorganized photos with no labels rarely helps. Instead, focus on submitting 10 to 25 strong, clearly labeled photos that directly support the issues in dispute.

Mistake 4: Making repairs without documentation

Emergency repairs are fine, but document everything before and during repairs.

Mistake 5: Aggressive accusations

Keep communications factual. If you later need escalation, your professionalism helps you.

FAQ: Denied Roof Insurance Claims in Oklahoma (State Farm Included)

Can State Farm deny a roof claim for hail damage?

Yes, State Farm can deny a roof claim if their inspection concludes there is no covered storm damage, the damage is excluded, or the damage is cosmetic only. Whether that conclusion is correct depends on policy language and documentation.

Do I need a leak for my claim to be approved?

Not always. Some roof damage can be covered even if interior leaks have not started yet. Policies vary, so documentation and policy language matter.

Can I request a second inspection after a denial?

Often, yes. In many situations, homeowners request reinspections after first submitting independent documentation. However, the process can vary significantly depending on the insurance carrier as well as the specifics of the claim.

What if State Farm says it’s “wear and tear”?

In many cases, a common response is to thoroughly document storm-related impacts, then clearly show consistent damage patterns and formally request a review. At its core, the dispute typically centers on storm causation versus, instead, alleged deterioration or wear and tear.

Will a contractor guarantee claim approval after a denied roof claim?

To be clear, no reputable contractor should ever guarantee an outcome. However, what a qualified contractor can do is provide thorough inspection documentation and maintain clear, professional communication to support a fair review.

When should I consider legal review after a denied roof claim?

Some homeowners consider attorney review when the denial appears inconsistent with evidence, when repeated reinspections fail, or when policy language seems misapplied. This is case-by-case.

Practical “Next Steps” Plan (What to Do This Week)

If your roof claim was denied in Oklahoma (including State Farm denials), here’s a clean plan:

Days 1–2

- Save the denial letter

- Request the full claim file (photos + report)

- Create a claim folder and timeline

Day 3–4

- Schedule an independent inspection

- Organize contractor photos and notes

Days 5–7

- Submit a reinspection request with attachments

- Ask for supervisor review if needed

- Keep everything in writing

If you need a deeper explanation of reinspection strategy and documentation, link internally to your Denied Roof Insurance Claims in Oklahoma City page.

schedule a free inspection today

Conclusion: a denied roof claim Is a Decision—Not a Verdict

While a roof insurance claim denial in Oklahoma can be discouraging, it is often based on limited documentation or a narrow interpretation of the damage. In response, many homeowners—including those insured with State Farm—choose to move forward by submitting organized evidence, maintaining clear communication, and making a structured request for review.

Your strongest leverage is not anger—it’s documentation.

If your denial doesn’t match what your roof actually looks like, your next step is simple:

document thoroughly, request review, and escalate professionally when needed.