Was your insurance claim denied?

If you have a denied insurance claim in Oklahoma City … that is not the end of the road.

Schedule your free inspection

Turn a Denied Roof Insurance Claims in Oklahoma City into a approval

If you live in Oklahoma City, you already know storms are not a “maybe” — they’re a certainty. Hail, wind, tornadoes, and heavy rain can roll through fast and leave behind damage that isn’t always obvious from the ground. You do the right thing: you call your insurance company, file a claim, meet the adjuster, and expect a fair outcome.

Then you get the letter:

“Your claim has been denied.”

Or worse: “Coverage is limited.” “Damage is cosmetic.” “Wear and tear.” “Maintenance issues.” “Not enough hail hits.” “Below deductible.” “No storm damage found.”

A denied roof claim can feel like a dead end — but for many homeowners in Oklahoma City, it’s not. Denials are common, and they are often reversed when you respond the right way with proper documentation, a reinspection strategy, and sometimes legal pressure when the insurance company refuses to follow the policy.

This guide breaks down:

- The most common reasons roof claims get denied in Oklahoma City

- The difference between cosmetic vs. functional hail damage

- The exact steps to take after a denial

- How a qualified contractor can strengthen your claim

- When bringing in an attorney can turn a denial into an approval

- Mistakes that can sabotage a valid claim

- Practical scripts and checklists you can use

If you want to learn more about full service options, see our Roof Replacement in Oklahoma City service page

Why Roof Insurance Claims Get Denied in Oklahoma City

Insurance companies usually deny claims for one of two reasons:

- They claim the damage is not covered (or is excluded), or

- They claim the damage is not caused by the reported storm

In reality, there are several common denial categories that show up again and again in Oklahoma City roof claims.

1) “Cosmetic Damage Only” (The Most Common Denial)

You’ll see language like:

- “Hail impacts are cosmetic.”

- “No functional impairment.”

- “Roof remains serviceable.”

- “No leaks observed.”

This is frustrating because hail damage can weaken shingles without causing immediate leaks. A roof can appear “fine” today but fail prematurely later. The insurance company may try to draw a line between appearance and performance, but that line isn’t always clear.

Functional damage may include:

- Fractured shingle matting

- Bruising that breaks the shingle’s integrity

- Exposed asphalt where granules were knocked off

- Cracking that spreads with heat/cold cycles

- Compromised sealing strips

- Wind-lift damage and creases

Even if the roof isn’t leaking right now, it can still be functionally damaged.

2) “Wear and Tear / Maintenance Issues”

You’ll see phrases like:

- “Long-term deterioration.”

- “Granule loss consistent with age.”

- “Brittle shingles.”

- “Improper ventilation.”

- “Old roof; not storm-related.”

Insurance policies usually exclude wear and tear — but that doesn’t mean they can ignore storm damage that occurred on an older roof.

A roof can be older and still suffer new storm damage. The real question becomes:

Can you prove the storm caused the damage being claimed?

That’s where documentation matters.

3) “Not Enough Hail Hits” / “No Storm Damage Found” This is a common tactic used by insurance companies to push denied claims in oklahoma city

Adjusters sometimes conclude:

- “No hail hits observed.”

- “Minimal hits; below threshold.”

- “Damage does not warrant replacement.”

But Oklahoma City neighborhoods can have highly localized hail. Two streets apart can experience very different storm intensity. If the adjuster did a quick inspection, they may have missed damage — especially on:

- North-facing slopes

- Soft metals (vents, flashing, gutters)

- Steeper or higher roof sections

- Areas shaded by trees that hide bruising patterns

4) “Below Deductible” or “Limited Coverage”

Sometimes it’s not a denial; it’s an underpayment. The carrier may agree there’s damage but claim the total is “below deductible” or offer repairs that don’t match what’s necessary.

Common issues:

- They pay for a few shingles when a slope is compromised

- They ignore collateral damage (vents, gutters, flashing)

- They undervalue labor, steep charges, or code items

- They exclude “line items” that are necessary to do the job right

Underpayment can be just as serious as denial.

5) Late Notice / Missed Deadline

Many policies include language requiring “prompt notice.” Some carriers take a strict stance on time.

Homeowners often delay because:

- No leaks are visible yet

- They didn’t realize damage existed

- They assumed it was “just cosmetic”

- A contractor didn’t inspect until months later

Late reporting can complicate your claim — but it doesn’t always kill it. What matters is how you document the storm event and the discovered damage.

6) Incorrect Storm Date / Causation Dispute

An insurance claim can be denied in oklahoma City by the carrier because…

- The storm date is wrong

- The damage predates the storm

- The storm wasn’t severe at your address

- Another storm is responsible

This is where storm data, photos, and inspection documentation help connect the dots.

schedule a free evaluation

Let us take a look at your denial and help you decide the best course of action.

Schedule your free inspection

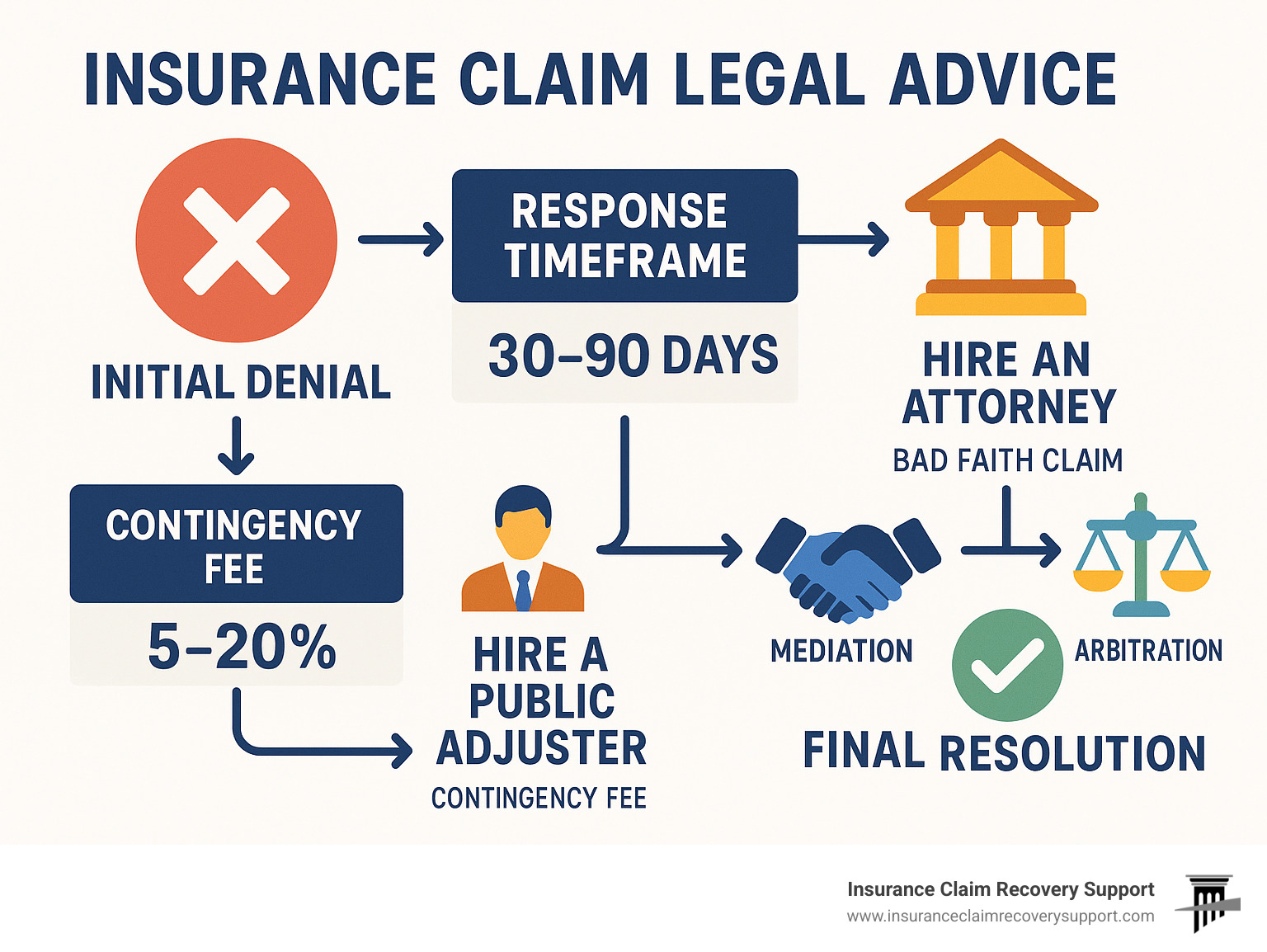

What “Denied” Actually Means (And Why It’s Not Always Final)

A denial letter is not the same thing as a court order. It’s the carrier’s position based on their inspection and claim handling.

In many cases, the denial happens because:

- The first inspection was rushed

- The adjuster missed functional damage

- The carrier is applying “cosmetic” logic too broadly

- The scope is incomplete

- The documentation presented was weak

- The carrier is trying to minimize payouts after storms

Plenty of Oklahoma City homeowners turn denied claims into approvals through:

- A stronger reinspection request

- Contractor documentation

- Appraisal or dispute processes

- Attorney involvement when needed

The quickest way to turn a denied insurance claim into a approval in oklahoma city.

Most successful reversals happen by following a simple strategy:

- Get the full claim file and identify the denial logic

- Get an independent inspection with detailed photo evidence

- Document functional damage and collateral indicators

- Submit a formal reinspection request with attachments

- Escalate to a supervisor/manager if needed

- If the carrier still refuses, consider attorney review or appraisal

Let’s break down each step.

Step 1: Request the Full Claim File and Denial Basis

Call your carrier and request:

- The adjuster’s report

- All photos taken

- Any measurements/notes

- The estimate (even if $0)

- The exact policy language they relied on for denial

You need to know whether they denied it because:

- “No damage found”

- “Cosmetic only”

- “Wear and tear”

- “Excluded cause”

- “Late notice”

- “Below deductible”

You can’t fix what you can’t see.

Step 2: Get an Independent Roof Inspection if you have a denied insurance claim in oklahoma city (Don’t Skip This)

A strong independent inspection should include:

- Photos of each slope

- Close-ups of suspected impacts

- Collateral damage photos (vents, soft metals, flashing, gutters, downspouts)

- Roof age indicators (without exaggeration)

- Ventilation notes (if the carrier blamed ventilation)

- Documentation of any wind damage (creases, lifted tabs)

- A summary that ties findings to the storm event

If your contractor only gives you “Yep it’s hail,” that is not enough. You need:

- A clear narrative

- Organized photo evidence

- Measurable documentation where possible

This is one of the biggest differences between an insurance claim that gets denied and one that gets approved.

(Internal link idea: Schedule a roof inspection in Oklahoma City → your service page.)

Step 3: Build a “Damage Story” the Carrier Can’t Ignore

Insurance companies live in documentation. Your goal is to create a clear, simple story:

- There was a storm on/around X date

- Your roof shows consistent damage patterns

- The damage includes functional impairment indicators

- Collateral components confirm the event (soft metal hits, etc.)

- The scope required is reasonable and consistent with roofing standards

If you can present a clean story with strong photos, you increase the odds the carrier reopens the claim or sends a more experienced adjuster.

Step 4: Request a Reinspection for a denied insurance claim in oklahoma city (The Right Way)

When you request a reinspection, don’t just say:

“Please reinspect, my contractor says it’s damaged.”

Instead, submit a short, professional request that includes:

- Claim number

- Storm date

- Summary of what was missed

- Attachments (photos + inspection summary)

- Request for a new adjuster or supervisor review

Example wording:

“Based on an independent inspection, we believe the initial evaluation did not fully document storm-related functional damage and collateral indicators. Please schedule a reinspection and supervisor review. Attached are photographs and a summary.”

Keep it calm, factual, and paper-trail-focused.

Step 5: Meet the Adjuster With Your Contractor (If Allowed)

Many homeowners get better results when:

- The contractor is present

- The contractor calmly points out specific areas

- The contractor sticks to facts and documentation

- Everyone stays professional

The best contractors don’t “fight” the adjuster — they document.

During reinspection, focus on:

- Marked test areas (if appropriate)

- Collateral components that show impacts

- Consistent patterns across slopes

- Any shingles that show fracture/bruising indicators

Step 6: If your insurance claim is denied in oklahoma city Escalate it Within the Insurance Company

If the reinspection still results in denial, ask for:

- A claims supervisor review

- A desk adjuster review

- A claim “re-evaluation” based on new evidence

- Written explanation addressing your submitted evidence

If the carrier ignores your evidence, that can matter later if you choose to escalate further.

How an Attorney Can Turn a Denied insurance claim in oklahoma city into a approval.

Sometimes a carrier only changes its position when it knows you are prepared to enforce the policy. That’s where an attorney can help — especially if:

- The denial seems unreasonable compared to the evidence

- The carrier refuses to re-evaluate or explain

- The adjuster report is sloppy or contradictory

- You suspect bad-faith claim handling

- The claim value is large enough to justify legal help

What Attorneys Actually Do in Roof Claim Disputes

A good insurance attorney may:

- Review the policy language and denial letter

- Identify misapplied exclusions or coverage interpretations

- Draft a formal demand letter requesting compliance

- Force clearer documentation from the carrier

- Push for appraisal or dispute resolution options

- Negotiate settlement terms

- File suit if necessary (in extreme cases)

Even one attorney letter can change how seriously a carrier treats your file, because it signals:

- You’re organized

- You’re documenting

- You understand the policy is enforceable

When You Should Consider Attorney Involvement if insurance denied your claim in oklahoma city

Attorney involvement is most helpful when:

- You’ve already provided strong contractor documentation

- The carrier is still refusing to fairly evaluate

- The difference in scope is significant

- You’re running into deadlines

- The claim is being delayed repeatedly without cause

Important: Not every denied claim by insurance in Oklahoma City needs a lawyer. Many get approved with a better reinspection package. But if the carrier is stonewalling, legal help can be a powerful lever.

How the Right Contractor Makes the Difference

Schedule your free inspection

Not all contractors help claims the same way.

Some contractors:

- Take vague photos

- Don’t organize evidence

- Don’t know what adjusters need

- Use overly aggressive language that backfires

- Focus only on “winning” instead of documenting

A contractor that helps convert denials into approvals typically:

- Produces organized inspection summaries

- Documents collateral indicators

- Understands common denial language

- Helps prepare reinspection packets

- Explains repair vs replacement scope clearly

- Communicates professionally with the carrier

What You Should Ask a Contractor Before You Rely on Them

Ask:

- “Do you provide a written inspection summary with photos?”

- “Do you document collateral damage (vents, flashing, gutters)?”

- “Will you meet the adjuster for a reinspection?”

- “Do you help create a reinspection packet?”

- “Do you understand cosmetic vs functional damage arguments?”

- “Do you follow Oklahoma code considerations where applicable?”

You don’t need a “loud” contractor. You need a thorough one.

Common Mistakes That Hurt Denied Roof Claims

Mistake 1: Only Taking “Far Away” Photos

You need:

- Slope photos

- Close-ups

- Multiple angles

- Consistent lighting where possible

- Clear context (what slope, what component)

Mistake 2: Waiting Too Long After Denial

Deadlines and carrier policies vary. The longer you wait:

- The harder it is to tie damage to a date

- The more likely the carrier claims “new damage” or “wear and tear”

- The more risk you face from additional storms

Mistake 3: Fixing Too Much Before Documentation

Emergency tarping is fine. But if you replace major components before the carrier documents them, disputes increase. If you must do repairs, keep:

- Photos before/during/after

- Invoices

- Material receipts

- Written explanation of emergency necessity

Mistake 4: Assuming the Adjuster Is the Final Decision-Maker

Adjusters often follow guidelines. Supervisors and desk reviewers may change outcomes when presented with better evidence.

Mistake 5: Getting Emotional With the Carrier

It’s normal to feel angry — but keep communications factual. Emotional calls often result in nothing but frustration. Documentation wins.

Denial Reasons Explained (And How to Counter Them)

“Cosmetic Damage Only”

Counter strategy:

- Document functional indicators (fracture, mat compromise)

- Provide collateral damage evidence

- Show consistent patterns across slopes

- Request written explanation of functional standard used

“Wear and Tear”

Counter strategy:

- Document storm-related impacts and patterns

- Provide photos showing fresh damage characteristics

- Show the roof was performing pre-storm (no leaks, etc.)

- Provide contractor report tying damage to storm mechanism

“No Storm Damage Found”

Counter strategy:

- Provide organized photos of impacts and collateral components

- Request a different adjuster for reinspection

- Provide storm date confirmation and neighborhood context

- Focus on slope-by-slope documentation

“Late Notice”

Counter strategy:

- Explain when damage was discovered and why it wasn’t visible earlier

- Provide inspection date documentation

- Keep narrative factual and consistent

- Ask carrier to show policy language and prejudice (how they were harmed by delay)

“Below Deductible”

Counter strategy:

- Compare scope line-by-line

- Identify missing items: steep, ridge, vents, flashing, gutters, code items

- Provide contractor estimate with documentation

- Request a supplement review

Turning a denied insurance claim in oklahoma city into a approval

Here’s a practical checklist you can follow:

Within 48 hours of denial:

- Save the denial letter (PDF)

- Request full claim file + adjuster report + photos

- Schedule independent inspection

After inspection:

- Organize photos by slope and component

- Create 1–2 page inspection summary

- Highlight 5–10 strongest photos, not 200 random ones

- Identify the denial reason and address it directly

Submit reinspection package:

- Email carrier with attachments (or upload if portal)

- Request reinspection + supervisor review

- Ask for written response acknowledging evidence

If still denied:

- Escalate to claims manager

- Consider appraisal/dispute options (if policy allows)

- Consult an attorney if stonewalling continues

FAQ: Denied Roof Insurance Claims in Oklahoma City

Can my insurance claim be denied because my roof is old?

Age alone shouldn’t be the reason if the damage is storm-caused and covered. But older roofs face more “wear and tear” arguments, so documentation becomes more important.

Do I need leaks for my claim to be approved?

Not necessarily. Many policies cover storm damage that functionally impairs the roof even before interior leaks appear.

Should I hire an attorney immediately?

Not always. Many denials reverse with stronger contractor documentation and a reinspection. But if the carrier refuses to fairly evaluate the evidence, an attorney can apply pressure.

Can a contractor really help get it approved?

Yes — if they document properly and present evidence clearly. The contractor’s inspection and photo package often becomes the backbone of a successful reinspection.

What if they only approve repairs but my contractor says it needs replacement?

That’s a scope dispute. A supplement, reinspection, or escalation process may resolve it. Documentation and line-by-line comparisons matter.

Schedule your free inspection

Conclusion: a denied insurance claim in OKLAHOMA city ISN’T the end… IT’S the start of a strategy.

A denied roof claim in Oklahoma City can feel personal, but it’s usually procedural: a rushed inspection, weak documentation, or a carrier interpreting the evidence in a way that reduces payout. Homeowners also have the right to file a complaint with the Oklahoma Insurance Department if a claim is unfairly handled.

The homeowners who get denials overturned usually do three things well:

- They document

- They respond quickly and professionally

- They escalate with evidence — and involve legal help if necessary

If you want help building a strong claim file and understanding your options, start with a professional inspection and clear documentation.

Internal links to add inside this post (recommended):

- Roof Replacement in Oklahoma City (cornerstone page)

- Hail Damage Roof Replacement in Oklahoma City (supporting page)

- Roof Inspection for Insurance Claims in Oklahoma City (supporting page)