Will Insurance Pay for Roof Replacement After Hail in Oklahoma?

If you own a home in Oklahoma, hail damage is not a matter of if—it’s when. After a major storm, many homeowners are left asking the same question: will insurance pay for roof replacement after hail damage in Oklahoma?

The short answer is: yes, insurance often will pay, but it depends on several important factors. Your policy type, the age of your roof, the extent of the damage, and how the claim is handled all play a role in whether your roof is approved for repair or full replacement.

This guide explains exactly how hail damage roof claims work in Oklahoma, what insurance companies look for, and how homeowners can avoid common mistakes that lead to claim denials.

Does Homeowners Insurance Cover Hail Damage in Oklahoma?

In most cases, hail damage is covered under standard homeowners insurance policies in Oklahoma. Because hail is considered a sudden and accidental event, it typically falls under covered perils.

However, coverage does not automatically guarantee full roof replacement. Insurance companies assess whether the damage meets their criteria for replacement versus repair.

Coverage depends on:

- Your policy type (ACV vs RCV)

- The severity and spread of hail damage

- Roof age and condition before the storm

- Local storm documentation

- Adjuster findings

Understanding these details upfront can prevent surprises later.

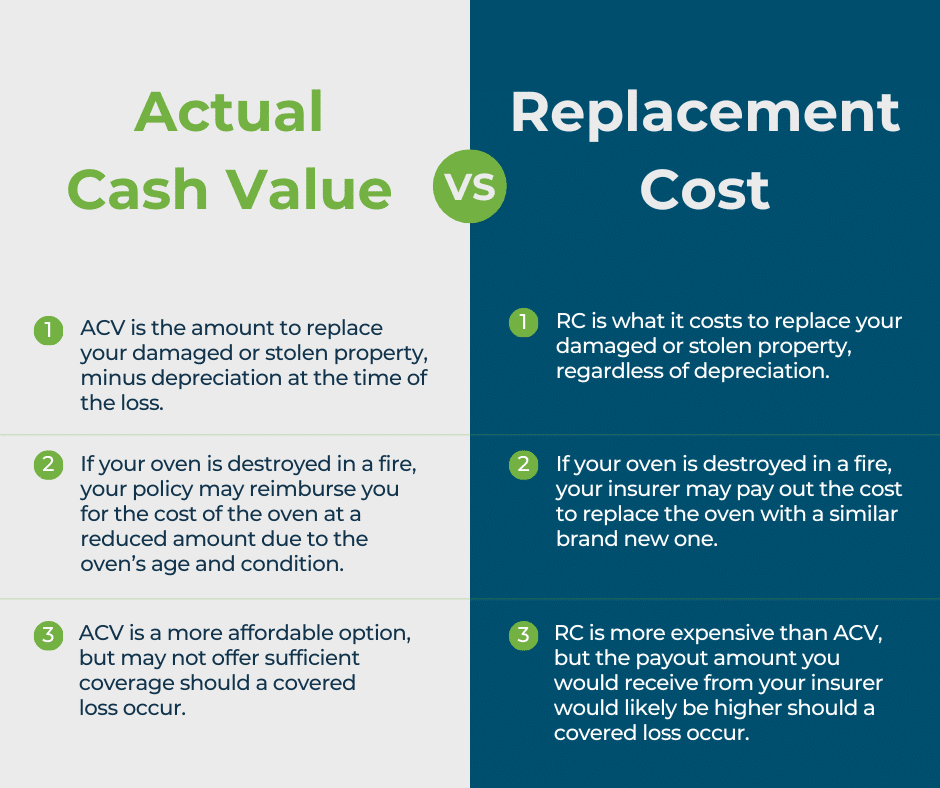

Actual Cash Value (ACV) vs Replacement Cost Value (RCV) Policies

One of the most important factors in whether insurance pays for roof replacement is your policy type.

Actual Cash Value (ACV)

ACV policies account for depreciation. That means:

- The insurer subtracts wear and age from the payout

- Older roofs often receive much lower settlements

- You may not receive enough to fully replace the roof

Example:

If your roof is 15 years old and expected to last 25 years, insurance may only pay a fraction of replacement cost.

Replacement Cost Value (RCV)

RCV policies are far more homeowner-friendly:

- Insurance covers the full cost to replace the roof

- Depreciation is initially withheld but paid after completion

- You only pay your deductible (in most cases)

RCV policies are far more likely to result in full roof replacement approvals.

What Kind of Hail Damage Qualifies for Roof Replacement?

Schedule a free inspection

Insurance companies do not approve roof replacement just because hail hit your area. The damage must meet specific criteria.

Common Signs of Qualifying Hail Damage

- Bruised or fractured shingles

- Granule loss exposing asphalt

- Soft spots from impact damage

- Cracked or broken tiles

- Functional damage affecting water shedding

Cosmetic damage alone may not qualify unless your policy specifically covers it.

Why Oklahoma Roofs Are Often Replaced After Hail

Oklahoma’s weather creates unique conditions that work in homeowners’ favor during claims.

Factors that increase approval rates:

- Frequent large hail events

- Strong documentation from storm tracking

- Known regional hail patterns

- Insurance carrier familiarity with Oklahoma storms

Adjusters expect hail claims in Oklahoma, which often leads to faster and more predictable outcomes compared to states with rare hail events.

Why Hail Damage Often Makes Roof Replacement Necessary

Hail damage doesn’t just affect how a roof looks — it affects how it functions. Even when a roof isn’t leaking right away, hail impacts can permanently compromise the materials designed to protect your home.

Below is why hail damage frequently leads to full roof replacement, not just repairs.

1. Hail Bruises the Shingle Mat, Not Just the Surface

Asphalt shingles are susceptible to Hail damage and are usually strong candidates for a full roof replacement after a storm. They are made with a fiberglass mat coated in asphalt and granules. When hail strikes, it can fracture or bruise the mat underneath, even if the shingle looks intact from the ground.

Once the mat is damaged:

- The shingle loses structural strength

- Water resistance is reduced

- The shingle becomes brittle and fails prematurely

This type of damage cannot be repaired — the shingle must be replaced.

2. hail damage can cause a roof replacement claim because of granule loss

Hail commonly knocks protective granules off shingles. Those granules:

- Shield asphalt from UV rays

- Control temperature

- Slow aging and cracking

When granules are lost:

- Sun exposure rapidly degrades the shingle

- Asphalt dries out and cracks

- The roof’s lifespan shortens dramatically

Widespread granule loss across multiple slopes usually meets insurance criteria for replacement.

3. Hail Damage Is Often Widespread, Not Isolated that is another reason insurance will pay after hail damage occures

Unlike wind damage, hail impacts entire roof slopes at once. This creates:

- Consistent damage patterns

- Multiple compromised shingles per slope

- Repair impracticality

Most manufacturers and insurance carriers agree that replacing scattered shingles across a slope does not restore the roof’s integrity.

4. Repairs Can Violate Manufacturer Guidelines

Shingle manufacturers require:

- Uniform installation

- Compatible materials

- Consistent aging and sealing

Spot repairs on hail-damaged roofs often:

- Break factory seals

- Prevent proper adhesion

- Void material warranties

When repairs compromise manufacturer requirements, replacement is the only compliant solution.

5. Hail Shortens Roof Life Even Without Immediate Leaks

A hail-damaged roof may not leak today — but damage often leads to:

- Accelerated deterioration

- Delayed leaks months or years later

- Higher repair costs down the road

Insurance policies are designed to address sudden, storm-related damage, not long-term deterioration. That’s why a roof replacement in Oklahoma City is often approved after hail events.

6. Insurance Standards Focus on Function, Not Appearance when determining roof replacement needs

Insurance adjusters evaluate:

- Functional damage

- Water-shedding ability

- Structural integrity

If hail damage prevents the roof from performing as designed, cosmetic appearance becomes irrelevant. Functional failure triggers replacement eligibility.

7. Mismatched Repairs Reduce Roof Performance

Even if replacement shingles are available:

- Color mismatches absorb heat differently

- New shingles age differently than existing ones

- Seal lines may not bond properly

This creates weak points and uneven performance, which insurers and manufacturers seek to avoid.

8. Oklahoma Hail Is Larger and More Impactful

In hail-prone regions, hailstones:

- Strike with greater force

- Create deeper mat fractures

- Damage multiple roof components

This increases the likelihood that replacement, not repair, is the safest and most durable option.

Bottom Line

Hail damage compromises a roof in ways that often cannot be fixed with spot repairs. When:

- The shingle mat is damaged

- Granules are lost

- Damage is widespread

- Manufacturer guidelines are violated

Full roof replacement is the only way to restore proper protection.

That’s why insurance companies frequently approve roof replacement after significant hail events — especially when damage is properly documented.

How Insurance Adjusters Decide Repair vs Replacement

Insurance adjusters evaluate:

- Number of damaged shingles per slope

- Spread and consistency of damage

- Manufacturer repair limitations

- Local building code requirements

If repairs would:

- Compromise the integrity of the roof

- Leave visible mismatching

- Violate manufacturer guidelines

Then full replacement is often justified.

Roof Age and Its Impact on Insurance Claims

Roof age is a critical variable.

- Newer roofs (0–10 years): Higher approval likelihood

- Mid-age roofs (10–15 years): Case-by-case

- Older roofs (15–20+ years): Often ACV-limited

That said, severe hail damage can override age concerns, especially if the damage is widespread and clearly storm-related.

Common Reasons Hail Damage insurance Claims Get Denied

Many homeowners don’t realize that insurance claims get denied for reasons that have nothing to do with actual roof damage.

Frequent Mistakes Homeowners Make

- Waiting too long to file a claim

- Allowing unqualified inspections

- Accepting adjuster findings without review

- Repairing damage before inspection

- Filing claims without contractor documentation

Insurance companies rely heavily on documentation. Without it, even legitimate damage may be undervalued or dismissed.

The Role of a Professional Roof Inspection

A professional inspection:

- Identifies damage adjusters may overlook

- Documents impact marks properly

- Uses photos and measurements insurers expect

- Helps align scope with replacement standards

An experienced contractor understands how hail damage presents on Oklahoma roofs and how to document it correctly.

This inspection becomes a critical part of your claim file.

Filing a Hail Damage Roof Claim in Oklahoma: Step-by-Step

- Schedule a professional roof inspection

- Confirm storm date and damage evidence

- Contact your insurance company

- File the claim promptly

- Meet the adjuster during inspection

- Review scope of work carefully

- Complete repairs or replacement

- Recover depreciation (RCV policies)

Skipping steps increases the risk of underpayment.

Deductibles and Out-of-Pocket Costs

In Oklahoma, deductibles are often:

- Percentage-based (1%–2% of home value)

- Separate wind and hail deductibles

Insurance typically does not cover the deductible, but reputable contractors structure projects to keep homeowner costs predictable.

Be cautious of any contractor offering to “waive” deductibles—this can create legal and insurance complications.

How Long Do You Have to File a Hail Claim in Oklahoma?

Most policies allow 12 months from the date of loss, though some allow more time.

Waiting reduces:

- Claim credibility

- Availability of storm data

- Adjuster flexibility

It’s always better to inspect early, even if you’re unsure about filing.

Will Insurance Cover Code Upgrades?

In many cases, yes—if your policy includes ordinance or law coverage.

This may include:

- Decking upgrades

- Ventilation improvements

- Drip edge installation

- Ice and water barriers

Without this endorsement, upgrades may come out of pocket.

Can Insurance Deny a Claim Based on Pre-Existing Wear?

Insurance does not cover:

- Normal wear and tear

- Poor installation

- Maintenance issues

However, hail damage is separate from wear, even on older roofs. Proper documentation helps separate storm damage from aging.

Why Local Expertise Matters in Oklahoma Hail Claims

Oklahoma storms produce:

- Larger hail sizes

- Short, intense impact patterns

- Mixed wind-driven damage

Local professionals understand how these storms affect roofing materials and how insurers evaluate damage in this region.

Generic inspections often miss Oklahoma-specific damage patterns.

Should You File a Claim If You’re Unsure?

Yes—get an inspection first.

Schedule a free inspection

A professional can tell you:

- Whether damage is claim-worthy

- The likelihood of replacement approval

- If filing makes financial sense

Filing unnecessary claims can impact your insurance history, so guidance matters.

Final Answer: Will Insurance Pay for Roof Replacement After Hail in Oklahoma?

In many cases, yes.

Insurance frequently pays for roof replacement after hail damage in Oklahoma when:

- The policy includes hail coverage

- Damage is properly documented

- Replacement is justified over repair

- The claim is handled correctly

The key is understanding the process and working with professionals who know Oklahoma hail claims inside and out.

Need Help With a Hail Damage Roof Claim?

If you suspect hail damage or want to understand your options, a professional inspection is the safest first step.

Learn more about our roof replacement services in Oklahoma City and how we help homeowners navigate the insurance process from inspection through completion.